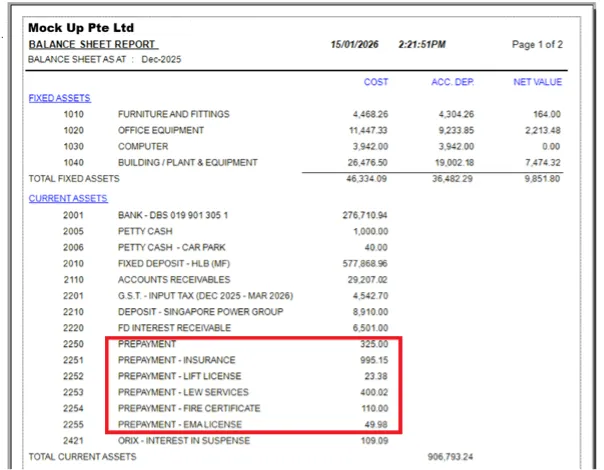

Below is a typical balance sheet that we want to focus on the current asset

Notice that we present the most liquid items first , i.e. the bank and cash balances, followed by the accounts receivables, other receivables and the non cash items example, prepayments, undue interest will be the last.

We also choose to present the various prepayments as individual line items as it provides clarity to the stakeholders contrary to usual practice that a separate schedule be prepared.

Notice that A/c 2250 is a combination of a few prepayment items prepared by the previous accounts staff, as compared to the detailed prepayments that we are handling.

Owners who read this Balance sheet will understand that these items are already paid over the next few periods and are accounted for.

As this is a management report, we are not concerned about the length of the balance sheet or too many items in the balance sheet, knowing that owners will conveniently not refer to the schedules, thereby , missing out the figures that were reported.

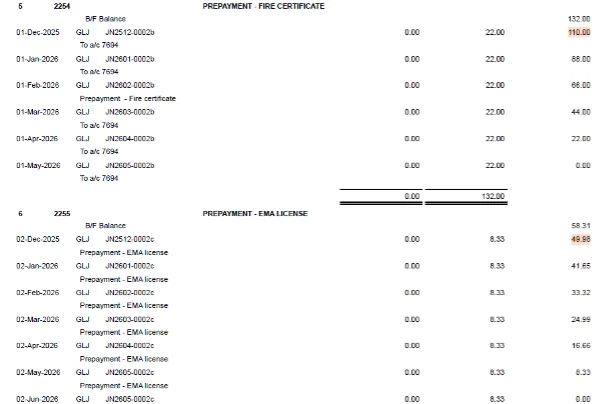

We also journalised all the entries until end of the period to become zero, at the same time when we recorded the payment against the supplier’s invoice, and during each reporting month, highlighted the end balance of the prepayment ledger as part of the schedule.

This will be save time to the monthly review to reconcile the prepayments